Investing for Children: It’s Not About the Account

Parents have more ways than ever to invest for their children’s future. But more options haven’t made the decision easier, just more nuanced. For nearly three decades, the menu of options available to parents has been relatively consistent: custodial accounts, 529 plans, Traditional IRAs, and Roth IRAs. This year, a new option has entered the conversation: Trump Accounts.

While new, this addition doesn’t fundamentally change how someone should approach the decision to open one or multiple types of accounts. The core tension remains the same: balancing tax advantages with flexibility.

Oftentimes when I meet with a client or prospect and the conversation pivots to save for college, they’ve already concluded they need a 529 account. They just want to know how to invest the proceeds. However, prior to talking about investing, I ask a rendition of these four questions:

Do we think the child will qualify for federal student loans?

Is the primary intent for these funds to be used for education?

Is it possible the child will pay for all or a significant part of their education with a merit scholarship, military scholarship, or sports scholarship?

How important is it to preserve flexibility if that plan changes?

The answers to these questions guide us to the ideal account or accounts to open. Let’s start with 529 plans as an example.

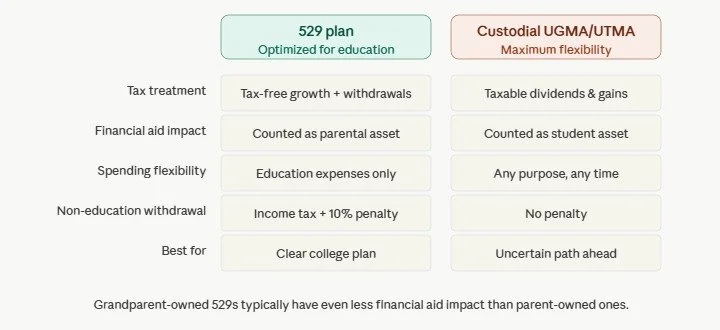

529 Plans

529s are excellent accounts if the answers to my first two questions are, “Yes.” The accounts are designed to be tax-advantaged investment vehicles to pay for school through tax-free growth and tax-free withdrawals for qualified education expenses. Some states even encourage parents to invest in 529s through income deductions or credits. Most importantly, 529s are treated as a parental asset for financial aid purposes, which generally has a much smaller impact on eligibility than student-owned assets like custodial accounts. In many cases, accounts owned by grandparents may have even less impact.

For example, let’s look at two students. Both are from low-income families and would qualify for federal student loans due to their family’s limited income. However, one student has a 529 that their grandparent opened. The other student has a custodial UGMA/UTMA account that their grandmother opened for the student’s benefit. The student with the custodial account may significantly reduce eligibility for need-based financial aid, since the account is treated as a student asset that can be used for education. Despite the 529 being allocated to the other student, it is not viewed as a student asset and does not have an impact on their loan eligibility.

When the plan is clear, the tradeoff is worth it. You are giving up flexibility in exchange for a very specific and valuable tax outcome. However, the more ambiguity there is around questions two through four, the larger a role custodial accounts may play in a client’s plan.

Custodial Accounts: UGMAs/UTMAs

Consider a possible scenario where a family spends years contributing to a 529 college savings account, carefully setting money aside with the expectation that it will be used for tuition. But when the time for their child going to university comes around, the outcome looks different. The child earns a scholarship, decides to attend a lower-cost school, or chooses a different path entirely whether that be a trade, the military, or entering the workforce right away.

Either way, the need for the 529 account is gone or significantly reduced. If the family wants to withdraw funds from the plan for non-education expenses, they are very constrained. What was once a highly efficient savings vehicle now has a gatekeeper with the toll for access being taxes on earnings at ordinary income rates and a 10% penalty.

The only non-taxable options are:

Assign a new beneficiary: This assumes there is a child or very well-loved family member who needs additional savings for education.

Convert up to $35,000 to a Roth IRA: A new option to deal with excess 529 funds, subject to certain limitations and timing requirements. However, Roth IRAs have their own limitations that make them difficult to access without penalties prior to retirement.

These are the situations where a custodial account can shine. The custodial account acts like any normal taxable investment account, but for the benefit of the child. Dividends, interest, and realized gains in the account are taxable in the years realized. Though the account is less tax efficient than a 529, index funds and ETFs (Exchange Traded Funds) dramatically reduce taxes compared to common actively traded mutual funds in past decades.

If a child goes to college, they can liquidate holdings in the account to pay for tuition. If they receive a scholarship of some sort and don’t need the money, they can use the funds in the account for a future down payment on a house, continue to let it grow, or pursue opportunities. The point is that it can be used for a wider range of savings and spending needs than a 529 plan.

Retirement & Trump Accounts

This brings us to what I’ll call our post-scarcity accounts, because it doesn’t make much sense to help your kid get a jump start on retirement unless their near-term needs and your own retirement are on track.

There are traditionally two retirement accounts parents can contribute to for their kids as long as the child has earned income:

Traditional IRAs

Roth IRAs

In practice, Traditional IRAs are rarely used for children. The decision between Traditional and Roth comes down to tax rates. If your tax rate today is higher than it will be in the future, Traditional may make sense. If it’s lower today, Roth is typically the better choice.

For most children, their tax rate today will be the lowest of their lifetime, which makes Roth IRAs the more logical option. However, while the Roth offers tax-free growth and withdrawals in retirement, its limitations on access mean it’s often better viewed as the capstone to a child’s investment plan rather than the starting point.

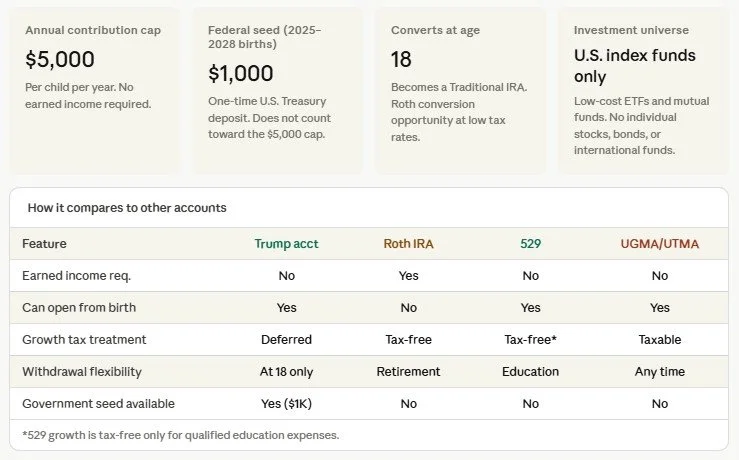

However, this is where the new Trump Accounts offer an interesting alternative for those with retirement planning in mind for their kids. Trump Accounts combine elements of 529 plans and retirement accounts by allowing contributions from birth while maintaining a long-term retirement focus. Historically, the earliest someone could begin saving in a tax-advantaged retirement account was when they earned income. Trump Accounts move that timeline forward.

With a maximum contribution of $5,000 per year, this allows tax-deferred growth to begin potentially a decade or more earlier than most people start saving for retirement. Over long periods of time, that difference can be meaningful. In practice, this means Trump Accounts aren’t a replacement for 529s or custodial accounts. They’re a complementary tool most useful for families who have already addressed near-term goals and want to extend planning across generations.

Let’s look at an example to see the potential implications. Assume a family contributes $2,000 per year to their child’s Trump Account. At age 18, those contributions and an annualized return of 8% lead to the account being worth $68,000. Also, at age 18, the Trump Account turns into a Traditional IRA. Since the young adult will likely be in the lowest tax bracket of their lifetime, it may create an opportunity to convert those funds into a Roth account at a relatively low tax rate where future growth and retirement withdrawals will be tax-free. If that 18-year-old has an effective tax rate of 12%, they may convert nearly $60,000 into the Roth account. If the Roth account continues to accrue at 8% per year until they turn age 60, they could have a tax-free retirement account worth over $1.5 million. Of course, this assumes rules stay the same, market returns, and disciplined follow-through.

Final Thoughts

In many ways, choosing the right investment account for children is less about the dollars contributed and more about direction. When the path is clear, it can make sense to optimize for specific outcomes. When it’s not, flexibility becomes more valuable. Either way, whether through a 529, custodial account, Roth IRA, or Trump Account, the objective remains the same: to give the next generation not just resources, but optionality. And to pass along the values that made those opportunities possible in the first place.

Addendum: One important limitation of Trump Accounts is their tax treatment. Contributions made by individuals generally use after-tax dollars and establish basis in the account, so those contributed dollars are not taxed again when distributed. However, the account’s investment earnings are generally taxed as ordinary income when withdrawn or converted. This can make Trump Accounts less tax-efficient than a Roth IRA, where qualified growth is tax-free, and potentially less favorable than a custodial account, where qualified dividends and long-term capital gains may receive preferential tax rates.