Jurassic World Part III: Net Present Value

Past articles in series: Part 1 and Part 2.

Nearly ten years ago I embarked on a quest to determine if Jurassic World would be a profitable investment. To determine Jurassic World’s profitability, I made the assumption that we are examining the project as “in-universe” investors in the year 2001.

To determine whether the project would be successful we’d use a Net Present Value analysis. A Net Present Value analysis begins with assigning the initial costs to a project, determining the operating cash flows, and then discounting cash flows to the present to determine if the investment has a positive expected value.

Funny enough, determining initial costs and operating cash flows is the most work intensive part of a Net Present Value analysis. Putting the equation together and applying a discount rate is simple. What always stumped me was determining what the discount rate should be. The discount rate is important because it represents the return an investor requires given the risk of the investment, the time value of money, and the opportunity cost of investing capital elsewhere. So nearly a decade later, the final part of our Jurassic World series will determine a reasonable discount rate, whether Jurassic World was profitable on an ongoing basis, and whether investors lost money when the park closed in 2015.

Discount Rate

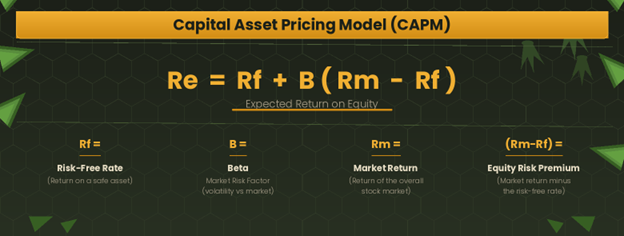

Finance textbooks often use the Capital Asset Pricing Model (CAPM) to determine a discount rate, but in practice many analysts rely on weighted average cost of capital, industry norms, or a required hurdle rate, particularly when the project is unusual or difficult to compare to public investments. I’m still going to use CAPM because it introduces some interesting discussion points. Below is the formula for CAPM:

Risk Free Rate: For the risk-free rate we will use 5.16% which was the yield on the 10-year U.S. treasuries in January 2001. The 10-year is used because it is liquid, widely quoted, and long enough to reflect long-term investments.

Beta: Beta reflects a company’s volatility compared to the market. A beta of 1 means a company’s volatility is the same as the broader market’s volatility. A beta below 1 means a company is less volatile than the market and a beta above 1 means it is more volatile. For our Jurassic World analysis, we run into two problems.

Jurassic World is a new project so it doesn’t have financial history we can use to assign a beta compared to the broader market.

There aren’t any other dinosaur theme parks we could use as a reference point.

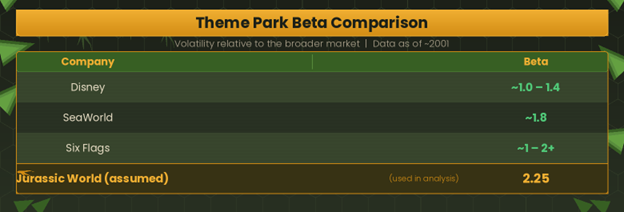

Therefore, we’ll look at the betas for theme parks and marine parks. Zoos are left out because they are not publicly traded. In this case, I’m using Disney, SeaWorld, and Six Flags for my data set.

Disney has a beta around 1.0–1.4, SeaWorld around 1.8, and Six Flags has ranged from below 1 to over 2 depending on the period. Because Jurassic World would be a single, highly risky project with no diversification, I assumed a beta of 2.25, which was the highest beta reported under Six Flags.

Market Return: An index of global publicly traded companies historically has had an annualized return of around 10% so we are going to keep things simple and use 10%.

Putting all of those pieces together, we arrive at a discount rate of 16.05%.

Net Present Value: Going Concern

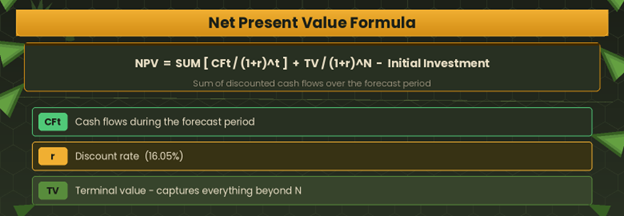

The next part of our analysis is determining if Jurassic World would have a positive expected value if ran as a park indefinitely. Below is the Net Present Value formula at its simplest:

For the forecasted period I am using the three years of construction plus an additional ten years of operations. Cash flow in this case is revenue minus expenses while incorporating a depreciation tax shield. Going back to Part II of this series, to account for the tax benefits of depreciation, I assumed the initial $3.1 billion investment is depreciated evenly over 10 years. This is a simplification and real-world assets would be depreciated over varying timeframes and often using accelerated methods. However, it captures the key economic impact: depreciation reduces taxable income and creates a meaningful tax shield.

When reviewing my past work, it was funny to see that I did not include growth in revenues or expenses year-to-year. I’ve updated my assessment to better reflect how real businesses behave.

Revenue growth is unlikely to be constant, as businesses typically experience strong early demand before gradually normalizing toward inflation-like growth as they mature. These assumptions reflect that pattern:

8% growth for operating years 1–5

6% growth for years 6–10

4% when calculating terminal value

I have expenses growing at 2.5% throughout the existence of the park, reflecting a combination of inflation and operating efficiencies.

Below is a chart showing the present value of cash flows for each construction year, ten years of operations, and terminal value. The Net Present Value is calculated by summing the present value of all projected cash flows, including the terminal value, resulting in an NPV of over $9.5 billion.

Net Present Value: Start to Closure

Now, as all of us who watched Jurassic World know, investors did not continue to receive profits from Jurassic World after 2015. This is because the park was closed after the Indominus Rex escaped in May 2015. So, while Jurassic World had a positive expected value “in universe,” what was its actual realized value?

I determined that Jurassic World was still in the red by over $850 million when it was shutdown. This means all of Jurassic World’s positive value is gained from cash flows that occur after our forecasted period. In other words, the investment only works if everything goes right for a very long time. Tough luck for our InGen and Masrani Global investors.

Final Thoughts

There is one major question I have today that I did not think of back in 2017 when I started this project, “Is Net Present Value the correct tool to determine whether Jurassic World is a worthy investment?”

My answer today is no or at least not on its own.

Net Present Value suggests Jurassic World was a highly attractive investment on paper. But in reality, that value only materializes far into the future, and the path to get there is anything but certain. The limitation of Net Present Value is not that it is wrong, but that it assumes a relatively fixed and predictable path forward.

In reality, the uncertainty of real business ventures creates both risks and opportunities, and traditional NPV captures the former much better than the latter.

For starters, it is missing out on a total return. Jurassic World would be valued at a multiple of its earnings and its earnings multiple may expand as it becomes more successful.

More importantly, it does not capture flexibility. Jurassic World would present management with a series of decisions over time, each with meaningful economic value. If the park is successful, the company could expand globally or increase pricing. If it struggles, operations could be scaled back or abandoned. And we can’t forget about all the merchandising rights!

Additionally, Jurassic World could lead to entirely new business lines, such as pharmaceuticals or genetic research which has been referenced in the most recent film.

So, would Jurassic World be a good investment? I wouldn’t be able to recommend Jurassic World as an investment unless the investor was comfortable with extreme uncertainty and a long wait for value that may never fully materialize. On the other hand, as a lifelong dinosaur enthusiast, I would join InGen’s investor group with an enthusiastic roar. Assuming they accept non-accredited investors and I updated my life insurance before stepping on the island.