Mistakes I've Seen

A client recently sent me an article about the mistakes an investor had made over their lifetime and then asked me about the mistakes I have made or seen. When I started to reflect on my mishaps, I quickly realized I’m a boring subject. I grew up talking about personal finance my entire childhood so I’ve always known best practices and when I strayed from the path in my early 20s, I didn’t have enough money to call my stock picking a mistake. Fortunately, I’m a financial advisor so the public can step in for my boring nature.

Starting Later in Life

Some people think you need a lot of money or to achieve a very high rate of return to be a successful investor. Those things are nice, but I think the greatest asset is time. In our example we have three investors. All are contributing $5,000 a year and receiving a hypothetical pre-tax portfolio return of 7%. The difference between the investors is the age they started investing and the total dollar amount contributed. As you can see, there is a stark difference between starting your investing journey at 45 and even 35 vs beginning at 25. What’s incredible is that the difference between lifetime contributions, that is money invested each year, is not significant.

When we look at “Tom” and “Bob,” Tom only invested $50,000 more than Bob over his entire lifetime. However, Tom’s portfolio ended up being worth nearly $1 million vs Bob’s $472K. That entire difference can be attributed to the compounding returns generated by the market from Tom’s early contributions. If Bob and Susan want to match Tom’s ending portfolio value, Bob would need to contribute $10,567 each year for thirty years and Susan would need to contribute $24,348 annually for twenty years.

Too Conservative a Portfolio

There are two things a portfolio needs to do throughout your lifetime: grow and manage risk. When we are in our working years, we want our investments to grow at the highest responsible rate possible and during retirement we want to provide a return that beats inflation (to maintain purchasing power) and provides a sustainable withdrawal rate (the amount of money taken out each year vs the balance of accounts).

We manage risk by being globally diversified (removing the risk of any single company’s performance), using time to smooth out the volatility in stocks, and bonds to provide stability for withdrawals later in life (typically 5-15 years’ worth of withdrawals).

Those are the main ideas behind a good portfolio, but at least a few times a year I see a young person who, because of an investor risk questionnaire, has half their investments in bonds, or an older person who is 100% in bonds. This means the young worker is robbing themselves of a higher return and the retiree might be taking more risk because the bond portfolio can’t cover their withdrawal rate.

Too Aggressive a Portfolio

I don’t see this very often aside from people who have crypto investments, but I have plenty of friends who say, “More risk means a higher reward.” And that’s not entirely true. More risk means you should demand more of a reward before making an investment, but it doesn’t mean the reward is guaranteed. That’s before we even get to whether someone is calculating expected return properly. I suspect most people who say, “more risk means more reward” are taking an asymmetric risk or high risk for low reward. If you text and drive, you should know what I’m talking about.

Individual Stock Picking

I’ll separate stock picking between people who just want to take some money off to the side and have fun vs people who actively trade in and out of individual stocks. If you’re in the latter group, just stop. For starters, it is very difficult to beat the market. The below image is from S&P’s SPIVA report which shows the percentage of funds that underperformed their benchmark. These are very smart people and anywhere from 80-95% of them underperform.

This data is as of 12/31/2024

Second, I have not met a DIY trader who tracks their performance and reviews how they have done compared to an index over ten to fifteen years.

High Expense Ratios

If you are dealing with expense ratios, you’ve likely already decided that individual stock picking is a waste of time, and that you want to have diversification in your portfolio. However, not all mutual funds and ETFs are built the same. A Vanguard fund, designed to track an index, may be invested across hundreds of companies, and have an expense ratio of 6bps (0.06%). Another fund, invested in a few hundred companies, may have an expense ratio of nearly 1%, because it is actively managed. As noted in the SPIVA report, if active managers have such high underperformance rates, there is no reason to use them when less expensive funds are available.

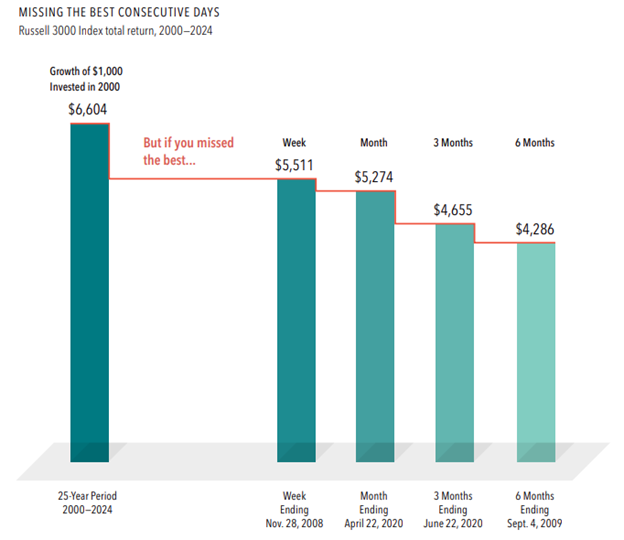

Market Timing

A common statement is stocks return 10% per year on average, however, there is a lot of “smoothing” to get to that 10% per year. As I noted a while back, the returns of 2021-2023 for the US (+26%, -19%, +24%) get you an average simple return of 10.33%. Things get even wilder when we look at the cost of missing the best weeks or months over a 20-year period (below chart). No one can predict the bottom or top of markets, so there is no point in trying. Instead, stay invested and rebalance according to your predetermined strategy.

Source: Dimensional Fund Advisors

Forgetting Taxes

Taxes come into play in several ways in a financial plan. When it comes to an investment portfolio, some mutual funds (typically actively traded funds) can have high percentages of capital gains distributions, which if held in a taxable brokerage account, get tacked on to your tax bill. This can surprise retirees in two ways: first is the tax bill and second, the capital gains can push a retiree’s adjusted gross income into IRMAA territory. IRMAA is the increase in monthly Medicare premiums for retirees with an adjusted gross income of $212,001.

Another is failing to consider how different account types are taxed. When a retiree unexpectedly needs money, the first account they typically look at is their IRA, which is often the worst account to take large sums of money out of since it has the highest tax consequences with distributions taxed at ordinary income rates. Even if an IRA is the only investment account someone has for a large distribution, it may make more sense to break up the distribution between two years and temporarily cover some of the balance with a line of credit.

Forgetting Estate Planning

Estate planning is a nuanced conversation where answers may change depending on the state you live in and how old your beneficiaries are. However, there are some near-universal guidelines such as keeping charities out of your will and instead listing them as beneficiaries on your IRA. Regardless of where you live, the objective of good estate planning should be to get the right assets to the right person/entity, at the right time in their life, and in the most tax efficient way possible.

Not Conducting a Spot Check

I’m not going to say everyone needs a financial advisor to manage their investment accounts, but if you are over forty-five years old, I think you should at least pay an advisor to conduct a retirement assessment every few years.

The idea behind getting a routine assessment is that you can make changes if you are not on track. And it is much easier to make those changes five to fifteen years prior to retirement than the year before. My favorite conversations are telling prospective clients they did everything right and they decide to work with us. The most deflating conversations are those when someone is less than a year out from retiring or had a major life event (divorce, death, etc.) and I must tell them the lifestyle they imagined is not sustainable with the assets and income sources they accrued. There is a lot you can change with ten years to prepare. There is very little you can change in three months.

Wild Cards

The last three on my list are not mistakes, but what I will call wild cards. Interesting circumstances that can add a challenge to a financial plan and are worth sharing.

Gray Divorce

There is a good chance if a couple over 60 decides to divorce and they are of normal middle to upper-middle class means, the divorce will significantly impact the lifestyle they expected to have in retirement. Clearly they’ve decided it’s worth the tradeoff, but gray divorce brings three main challenges to a financial plan:

Fixed Expenses: Many expenses such as housing, utilities, and debt are fixed so when you’re single those expenses consume a larger percentage of your income than when you have two incomes. This often means people don’t have the discretionary spending they had envisioned.

Asset Selection: While assets may be split evenly between the two sides, not all assets are created equally. Sometimes people prefer to keep a home or property and give away a portion of their investment accounts instead. This can create a challenge or decision points for retirement planning because a home and other types of property are not income producing.

Time: The now-separated couple have only months, or a few working years left to accumulate the savings needed to generate the retirement lifestyle they expected. Honestly, unless you have a very high paying job and a career where you are more productive at the tail end of your career than the middle, you’re probably not going to hit your original lifestyle goals.

Not Spending Enough

If you didn’t get the deferred-gratification gene, you’ve got to work very hard to overcome that.” - Charlie Munger

I’m fortunate to work with many people who have saved diligently over many decades and now have a significant amount in investments. One of the things I’ve noticed is that people rarely switch from great savers to spenders. This is a shame because retirement assets reflect a lifetime of good decision making and deferred gratification. Assets should be deployed to buy experiences a client has spent their life dreaming about. The sad thing is if a retiree doesn’t use that money to fulfill their dream, their beneficiaries will have no problem using it.

Large Unrealized Gains

For some reason I find individual stocks with large unrealized gains to be funny. They remind me of the very fancy china sets that sit in the armoire of a grandparent’s house: you can’t use it, and the kids are going to sell it when the grandparents die.

Large positions in a single stock are often too tax inefficient to tap outside of an emergency (though useful for securing lines of credit) so families often just wait for the step-up basis after death to diversify into other assets.