Life Finds a Way

A client letter and video essay 65 million years in the making. Every now and then our team includes a client letter reviewing the fundamentals of investing alongside our standard quarterly market review. A couple of the topics I have wanted to address for some time is the role preparation and turbulence play in investing. A recurring theme of mine is when it comes to humans, there is nothing new under the sun. 2,500 years ago, Sun Tzu said, “Every battle is fought, before it is won.” If you grew up playing sports or spent time in the military, you’re familiar with the adage, “train like you fight/play.” Investing is no different. Making the right choices today (training) will make you better prepared for the battle (market downturns or recessions).

Blue the Velociraptor

Turbulence comes from my love of Jurassic Park. There is an adage that, “bad luck comes in threes” and while I’m not superstitious, I think there is some truth there. Many parts of our life have “sensitive dependence to initial conditions.” A single thing we depend on, let’s say a loyal employee avoiding the temptation of corporate espionage, can go wrong, which leads to a cascading series of failures. If you’re not prepared, these series of events can overwhelm you and lead to ruin. However, if you prepare beforehand, that preparation will give you and other people time to adapt. And that’s what makes markets so effective. With little to no central planning they can adapt and thrive. If you like video essays, click the image of Blue the Velociraptor, otherwise, the letter is below.

2023 marks the 30th anniversary of Jurassic Park. For thirty years parents have been terrorized over the correct pronunciation of memorable dinosaurs such as Parasaurolophus and Brachiosaurus. More relevant, we’ve been graced with thirty years of Jeff Goldblum’s Dr. Ian Malcolm.

For those who need a quick refresh, Dr. Malcolm is one of the experts invited to tour Jurassic Park before its grand opening. While everyone else was impressed with the miracle of bringing dinosaurs back to life, Dr. Malcolm took a negative approach. Dr. Malcolm stated that the level of control Jurassic Park’s engineers were trying to exert over the dinosaurs was unsustainable. To borrow the parlance of chaos theory, Jurassic Park had, “sensitive dependence to initial conditions.” This meant that future changes to the system, no matter how small, would produce additional consequences that are magnified over-time.

An example of sensitive dependence to initial conditions might be your work commute. Those of us who’ve had to deal with a long commute eventually find the most efficient time to leave home. But if it takes you a couple extra minutes to find your keys (the initial condition), then you end up stuck at all the red lights, which puts you on the wrong side of the tracks for the morning train, and now you’re fifteen minutes late to work.

We also see sensitive dependence to initial conditions in the market. Case in point would be duration risk in Silicon Valley Bank’s bond portfolio. There we saw in the span of a week how a $1.8 billion post-tax earnings loss from mismatching bond duration with depositor needs, led to a call to raise capital, which torpedoed the bank’s stock, that led to a run on the bank with Venture Capitalists scrambling to get their money out, to Velociraptors devouring SVB’s shareholders. That last part didn’t make the news.

Sensitivity to initial conditions can create significant short-term volatility. This volatility can range from the very annoying when being late for work to terrifying when a stock is crushed. What I find interesting though is the following:

The way to overcome short-term volatility in investing is a lot like how we prepare for volatility in life.

The more time we have, the less we need to be concerned with short-term volatility.

Short-Term Volatility

Commentators act as if these dramatic declines are impossible to predict and they are correct. Short-term volatility is impossible to predict but eminently possible to prepare for. Most of us prepare for volatility every day. We build slack into our schedules and show up to meetings early. We pack extra clothes on trips or carry an emergency beacon while backpacking. Where we get in trouble is when risk mitigation turns into a complex formula to justify risk efficiency. Bear mace is unwieldy, and you have less than a 1% chance of encountering a grizzly on your Yellowstone hike. Why not streamline your hiking experience and leave that can of bear spray in the car? People too smart for their own good frequently take that approach when investing.

That’s not the perspective we have. When it comes to investing your portfolio there are two primary ways we prepare for short-term volatility.

Surplus Capital: We advise our clients to build and maintain a larger portfolio than needed than if they were to live on the razor’s edge of efficiency. Individuals can suffer from duration risk just like Silicon Valley Bank. We want to make sure there isn’t a mismatch between someone’s cash flow needs and what their portfolio can provide.

Bonds: We allocate enough money to the bond side of the portfolio to cover lifestyle needs until stocks recover and grow from the volatility.

As if anyone needs reminding, 2022 was not a good year for stocks or bonds, but it should not have caused a change in lifestyle. We prepare for short-term volatility.

More Time

What got me thinking about this topic in the first place is the fear we have when we identify a negative trend that is outside our control. I’m drawn to articles arguing the case for a looming debt crisis, rising interest rates, famine due to war, recession, arctic methane frying the planet like Mercury, etc. Often the initial analysis of doom seems plausible! Your mind starts to go down the butterfly effect of negative scenarios.

What I started to notice though is mine and everyone else’s grand negative predictions are almost always wrong.

For an example let’s examine our present societal fear, rising interest rates and market returns.

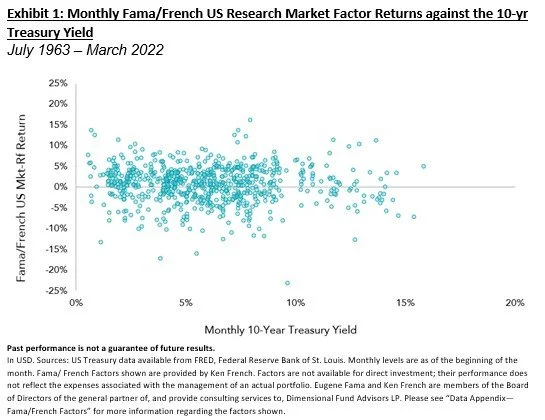

There are plenty of doom and gloom articles on how rising interest rates will be negative for the market and therefore individual investors. But if we are investors for the long-run, what I see is there is no correlation between yields on the 10-YR Treasury and market returns (Exhibit 1). There is also very little impact on market returns after consecutive rate hikes compared to no rate increases (Exhibit 2).

Why is this the case? Why is there little to no discernable impact years later? Why are our negative predictions less devastating than we assume? I think it’s because our fear of loss and uncertainty blinds us to positive butterfly effects.

Markets and people are adaptive. They take in new information, even negative information, and adjust to better their circumstances. To borrow Dr. Malcolm’s quote, “Life finds a way.” Every day eight billion people (admittedly, not always the same people) wake up to take part in actions they hope will ultimately better their lives. Business leaders try to increase shareholder value by providing customers with a better product or by improving efficiency. Consumers buy goods that they need or desire. Producers try to meet consumer demand. Individuals apply for jobs that will pay them the most for their utility. Countries negotiate optimal trade deals. Everyone is trying to better themselves and these cascading series of interactions in a market-based system, magnified over-time, trend towards making the world better for everyone.

This isn’t to dismiss hiccups and short-term volatility. For those who are not well capitalized, volatility can be devastating and ruinous. However, for those who prepare and have their eyes set on the long-run, life finds a way, and it generally finds its way towards positive returns.