Should You Give an Inheritance All at Once?

One of the challenges I help people navigate is estate planning. And I say I help clients navigate estate planning rather than solve the problem of estate planning because the plan often changes. One of the most common reasons an estate plan might change is concern about an heir’s ability to manage the inheritance.

That’s why I was excited to learn about a study titled Inheritance Dissipation and the Case for Time-Phased Estate Planning: An Empirical Assessment from HRS Data. Using Health and Retirement Study Data from 2010-2018, the researchers attempted to quantify how much an inheritor’s net worth changed.

For every $1 inherited, an heir’s net worth was calculated to retain only $0.61 of that inherited dollar the following year. In other words, if someone inherited $500,000 in 2025, the study’s average estimate suggests that their net worth in 2026 would reflect only about $305,000 of that inheritance.

Two Groups

As we all know, there is a lot of important information hiding in averages and this study is no different. Of the 3,005 participants, most could be sorted into one of two groups: 42% were spendthrifts and 43% were savers.

The spendthrifts, my word and not the authors, were defined as those whose net worth declined to its previous balance and trajectory after the inheritance. It is almost as if they never inherited the money in the first place. The savers on the other hand had at least a net worth that matched what they reported in the year of their inheritance.

The authors of the study ascribe some of the extreme inheritance spending to a strange psychological theory called Terror Management Theory. This is when spending is an avoidance response to the death-related source of funds. Their solution is time-phased distributions from the estate which simply means a portion of the estate will be given to the heir(s) at various intervals in time. For example, someone may receive 25% of their inheritance after they turn thirty, another 25% at thirty-five, and so forth.

I personally don’t find an inheritance to be too scary and subscribe more to Charlie Munger’s thoughts on spenders versus investors: “If you didn’t get the deferred-gratification gene, you’ve got to work very hard to overcome that.” However, I am a fan of staggering out when an heir has access to their inheritance, depending on the situation.

Why Stagger an Inheritance?

I think there are two main reasons to grant portions of an inheritance at predetermined phases.

The recipient is not ready to inherit the assets.

Protection from third parties.

This means even if an heir belongs in our “saver” category, it still may be beneficial to have a time-phased distribution for their inheritance.

Let’s begin with the first reason. For many of the people we work with, if they were to pass away, it’s not unreasonable to expect their heirs to receive an inheritance of $1 million or more. Now, it is one thing for someone in their fifties with their own 401(k) and plenty of life experience to inherit $1 million. It can be a different story when someone in their twenties inherits $1 million. In that case, it is perfectly reasonable to be concerned that a large part of the inheritance could be permanently impaired by overspending on items or experiences that don’t add material value.

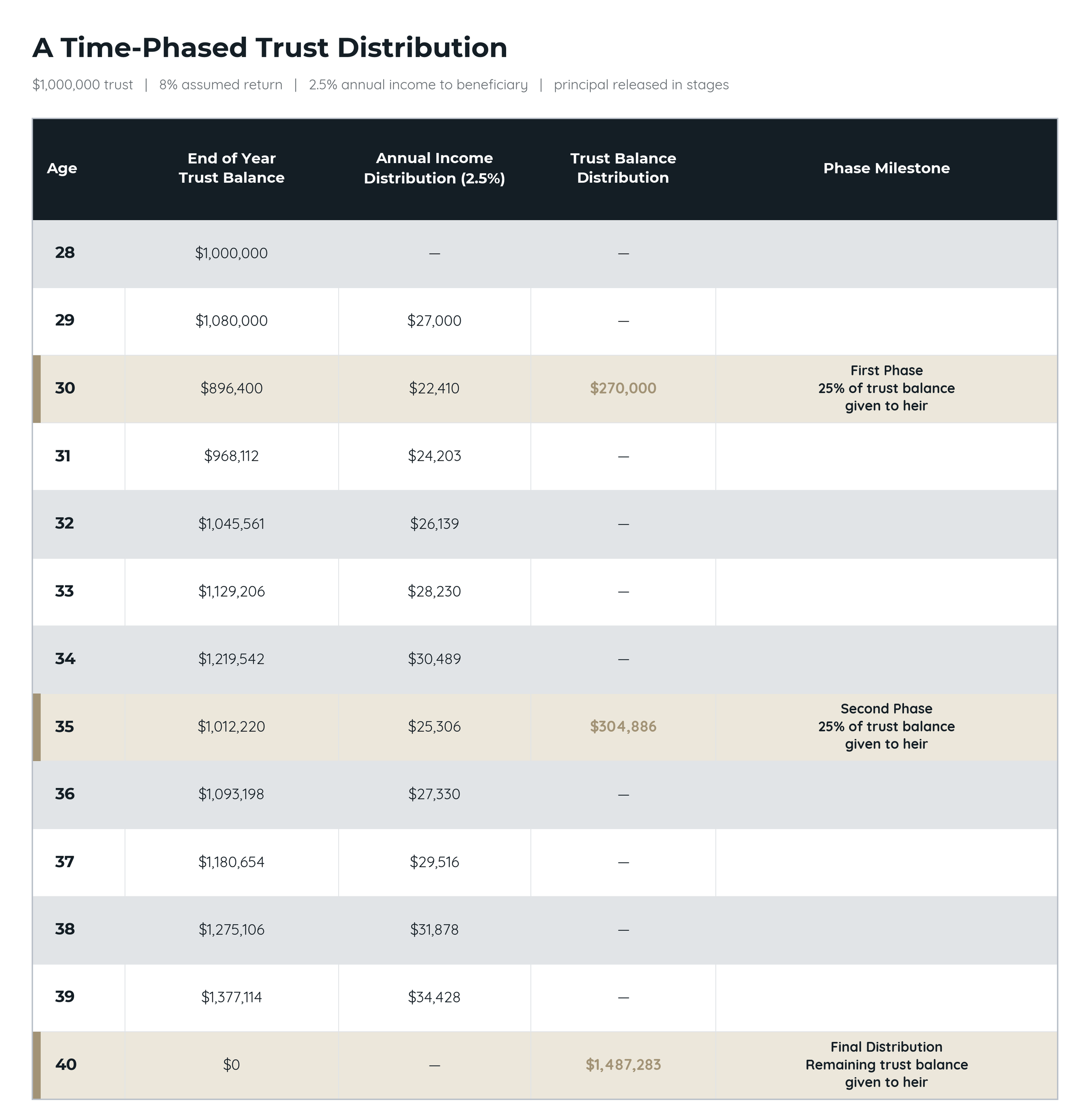

This is where staged distributions come in. To begin, the mechanism for staged distributions is a trust. So in our example, let’s have a hypothetical parent leave $1 million in trust for the benefit of their daughter. Their daughter is twenty-eight and the trust states the daughter will receive 25% of the current trust balance at age thirty, another 25% at age thirty-five, and the remaining balance at age forty.

If you follow along in the table below, you’ll see how this works in practice. Trusts have different tax brackets than individuals so income (dividends and interest) kept within a trust is often taxed at a very high rate. Rather than retaining that income inside the trust, the trustee may distribute the dividends and interest to the daughter, who would generally report the income on her own tax return. This means that, contrary to popular belief, an heir often receives income from the trust before the phased principal distributions begin.

Then at age 30, the daughter receives 25% of the current balance of the trust in addition to income for the year. The daughter continues to receive income from the trust for the following years, receives 25% of the trust balance at age 35, and finally the remaining balance at age 40. In my scenario, the trust at age 40 has significantly grown despite the prior distributions because the remaining assets continued to earn investment returns.

When people think about trusts they often think the money is under lock and key until the trust expires. This illustration shows the heir economically benefits from the trust to the tune of nearly $30,000 per year, has multiple opportunities to navigate large withdrawals before the final distribution, and has access to the trust for normal provisions such as health and education expenses.

The second benefit of phased distributions is that it gives the heir plenty of time to learn how to treat their inheritance regarding third parties. One person an inheritance may need protection from is a current or future spouse.

In this case there doesn’t need to be any malice involved. The simple fact is most people would prefer in the event of a divorce that the assets given to their children be kept by their children and not split up for the benefit of their ex-son or daughter-in-law.

Technically, assets gathered prior to a marriage and even gifts given or inherited during a marriage are treated as separate property. So, in the event of a divorce, those assets may remain separate property, provided they can be adequately traced and have not been converted into marital or community property. However, things can get messy when inherited assets are commingled with joint property.

What is commingling? It’s when assets gifted to someone are then used to purchase or make investments in joint property. For example, let’s say someone inherits $1,000,000. Over a period of years they periodically use the inheritance to fund a joint investment account with their spouse. Ten years later they file for divorce, and the value of the joint investment account has grown to $2.2 million.

In this situation it takes good record keeping as well as time-intensive forensic accounting to untangle how that joint investment account should be divided.

This is where a time-phased trust distribution plan comes in. For as long as the assets remain properly held and administered inside the trust, they are generally less susceptible to being commingled with marital property. The trust acts as a moat protecting the inheritance. And by spreading out distributions over time, it gives the heir an opportunity to learn about the various risks to their wealth and how they can be mitigated. The simplest lesson being that assets such as a house, investments, or property purchased with proceeds from the inheritance should be titled only in the name of the heir.

Conclusion

In my opinion, the goal of a trust should not be to control an heir from beyond the grave, but to give them the best opportunity to navigate their own financial journey. A time-phased distribution can provide that balance. The heir still benefits from the income and assets held in the trust, while gaining time to develop the experience needed to manage larger distributions responsibly. It also creates a period of protection during which the inheritance is less exposed to overspending, commingling, divorce, creditors, or other financial mistakes.

Ultimately, estate planning is an exercise in judgment. The question is not simply, “Who should receive my assets?” It is also, “When and under what circumstances will those assets do the most good?” A thoughtfully designed trust can help ensure that an inheritance becomes a durable foundation for the next generation rather than a temporary increase in their bank account.